HSA Overview

A health savings account (HSA) is a tax-advantaged savings account for healthcare expenses. You and/or your employer can contribute while you are covered by a qualified high-deductible health plan. Other eligibility requirements apply.

HSA contributions reduce your taxable income and help lower your taxes. Any investment growth is also tax-free for even greater savings. With an HSA, you get maximum tax savings while building a valuable source of money for expected—and unexpected—healthcare expenses.

Costs like deductibles, copays, prescriptions, over-the-counter medicines and drugs, and hundreds more can be paid tax-free from your HSA. HSA dollars can also be used to pay COBRA, Medicare, and retiree health insurance premiums. Non-medical withdrawals are allowed but they are subject to income tax, and a 20% tax penalty applies unless you’re disabled or over age 65.

Here are several more key points:

To make or receive HSA contributions, you must be enrolled in an HSA-qualified high-deductible health plan.

Annual contribution limits apply. If your employer doesn’t fully fund your HSA, you can make your own contributions through pre-tax payroll deductions.

You can use your HSA money anytime—now or build wealth for retirement.

Unused HSA funds roll over from year to year regardless of health plan coverage—no deadlines or use-it-lose-it rules to worry about.

An available investment lineup lets you invest your entire HSA balance—no minimum cash balance required.

Your HSA always belongs to you even if you change jobs, retire, become unemployed, switch medical plans, get married or divorced, or move out of state.

Have another HSA? No problem! You can transfer your other HSA balance to your Gallagher HealthInvest HSA. Simply complete and submit our HSA Transfer Request to your other HSA administrator or follow their instructions. Forms are available online.Log in and click Resources.

Triple Tax Savings

HSAs provide a unique “triple” tax-saving advantage:

Contributions made through payroll deduction or by your employer are tax-free;

Investment growth (if any) is tax-free; and

Withdrawals when used for qualified healthcare expenses are tax-free.

HSA tax savings include state income tax (most states) and federal income tax. HSA contributions made by your employer or through pre-tax payroll deduction are also exempt from FICA taxes (Social Security and Medicare). Individual situations vary, but most save up to 30% or more.

Example: Rowan and his spouse earn a medium income of $130,000 per year. They have two children and pay about 35% in combined taxes (state, federal, and FICA taxes). Rowan’s family is covered by an HSA-qualified high-deductible health plan through his employer.

Rowan has decided to contribute $300 per month to an HSA through pre-tax payroll deduction. This drops Rowan’s taxable income by $3,600 per year and will save him an immediate $1,247 in taxes.

Estimated HSA Tax Savings ($300/month Pre-tax Payroll Deduction)

| ||||

Taxable Income | Federal Income Tax1 | State Income Tax2 | FICA Taxes3 | Annual Tax Savings4 |

Low | 10–12% | 0% | 7.65% | $635–$707 |

Medium | 22–24% | 5% | 7.65% | $1,247–$1,319 |

High | 32–37% | 10% | 2.35% | $1,597–$1,777 |

1 Marginal federal income tax brackets for single and married filing jointly. 2 State income tax rates vary by state. Some states do not have a state income tax. HSA contributions may not be tax-exempt in certain states. 3 Social Security 6.2%; Medicare 1.45%. The Social Security portion of FICA taxes does not apply after meeting the wage limit for the given tax year. An additional 0.9% Medicare tax applies to those with earned income over $200,000 ($250,000 if married filing jointly). 4 These amounts are estimates. Individual circumstances vary. Your actual tax savings may be more or less.

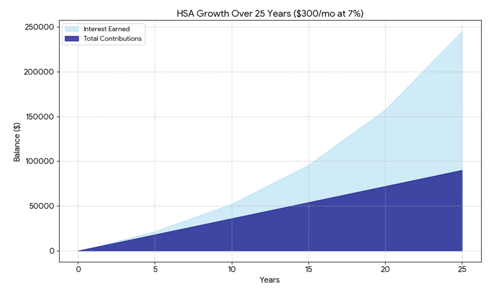

HSA Wealth Building

How $300 per month can become $240,000!

With triple tax savings, first-dollar investing (no uninvested cash balance required), and daily compounding, your Gallagher HealthInvest HSA provides an unbeatable long-term wealth building opportunity.

Example: At $300 per month, Rowan will have contributed $90,000 to his HSA after 25 years. Adding in around $150,000 of long-term investment growth, Rowan’s projected HSA balance could become as much as $240,000 or more—all tax-free! This hypothetical example assumes Rowan doesn’t touch his HSA money and earns an annual return of 7% (common assumption for stock market investments) with daily compounding. Individual situations vary. Stock market performance is not guaranteed.

“Gold-bell” Service Comes Standard

You work hard and deserve the best. Based on decades of experience, our proven system and processes deliver what we like to call “gold bell” service. Easy online self-service and personalized help when you need it are readily available. When the bell rings, we’re there!

Award-winning Customer Care. Our Customer Care Center has earned BenchmarkPortal’s Center of Excellence award every year since 2015.

Short Hold Times. We answer most calls within 30 seconds. If you need help, one of our capable representatives will quickly answer your questions or resolve your issue.

Easy Digital Services. Our proprietary system makes it easy to use and manage your Gallagher HealthInvest HSA.

User-friendly online portal

Handy mobile app, HRAgo® (for HSAs, too)

Free debit card for qualified purchases

First-dollar Investing. With Gallagher HealthInvest, you get to invest your entire HSA balance. Many HSA providers require a minimum cash balance (up to $2,000 or more) before you can start investing.

Insurance Shopping. Need help finding the best individual or family health insurance? Speak with an expert free of charge. Get personalized options in about 15 minutes. Licensed agent in all 50 states. Services provided at no added cost by Gallagher Alternative Health Insurance Solutions.

COBRA alternatives

Major medical, ACA-qualified plans

Medicare Advantage and Supplements

Dental, vision

About Your HSA

Your Gallagher HealthInvest HSA is easy to use, and it’s a smart way to lower your taxes. You can use your HSA dollars for a wide range of healthcare expenses for you, your spouse, and qualifying dependents—all tax-free.

Contribution Eligibility Requirements

Any eligible individual can make or receive contributions to an HSA. To qualify, you must be covered under an HSA-qualified high-deductible health plan (HDHP) on the first day of any month in which an HSA contribution is made or received. An HSA-qualified HDHP costs less than a traditional health plan, but it has higher annual deductibles and out-of-pocket maximums set by the IRS.

You must also meet the following requirements:

You have no traditional (non-HDHP) health coverage. Exceptions include certain types of permissible coverage, such as specific injury, accident, disability, dental, vision, or long-term care insurance.

You do not have a general purpose (full coverage) healthcare flexible spending account (FSA) or health reimbursement arrangement (HRA) coverage. Limited-purpose FSA or HRA coverage is allowed.

You are not enrolled in Medicare.

You cannot be claimed as a dependent on someone else’s tax return.

You do not receive health benefits under TRICARE.

You have not received Veterans Administration (VA) benefits within the past three months, except for preventive care. If you are a veteran with a disability rating from the VA, this preventive care exclusion does not apply.

Other conditions may apply. IRS Publication 969 contains more details.

Contribution Methods

If you qualify as described above, your HSA can be funded pre-tax by you, your employer, or both. After-tax contributions can be made by you or any other person.

Pre-tax Contributions. You can set up a pre-tax deduction from your paycheck. The amount can be changed or cancelled at any time. In some cases, your employer may make pre-tax contributions on your behalf. Pre-tax contributions are exempt from state income tax (most states), federal income tax, and Social Security and Medicare (FICA) taxes.

After-tax Contributions. Manual after-tax contributions can be made by check or electronically transferred from a bank account. After-tax contributions are tax deductible.

Contribution Limits

Your maximum HSA contribution amount depends mostly on whether your high-deductible health plan covers just you (self-only) or you and at least one other person, such as a spouse or dependent (family). The IRS sets annual HSA contribution limits (see chart below). Those age 55 and older are allowed up to an additional $1,000 “catch-up” contribution. IRS Publication 969 contains more details and examples.

Annual HSA Contribution Limits | ||

HDHP Coverage | 2025 | 2026 |

Self-only | $4,300 | $4,400 |

Family | $8,550 | $8,750 |

Monitor your total contributions regularly. You are responsible for making sure your total HSA contributions do not exceed the annual maximum. If your employer overcontributed, notify your employee benefits office immediately. If you overcontributed or need to lower your payroll deduction amount, use our Contribution Correction Request form. Forms are available online. Log In and click Resources.

Transfers & Rollovers

The transfer and rollover provisions described below allow you move money to your HSA from certain types of IRAs or another HSA.

One-time, Direct Transfer from an IRA. You can make a direct transfer from a traditional or Roth IRA (not a SEP or SIMPLE IRA) once in your lifetime. This is called a “qualified HSA funding distribution.” The amount transferred, plus any other HSA contributions you make or receive in that tax year, cannot exceed your annual HSA contribution limit. You must remain eligible to contribute to an HSA for 12 months following the transfer. If you fail to meet this requirement, the transfer amount will be treated as taxable income and become subject to a 10% penalty. The transfer must occur directly from your IRA to your HSA. To make this type of transfer, contact your IRA administrator for instructions.

Direct Transfer from Another HSA. You can transfer funds directly from another HSA, if you have one. There is no limit on the number of HSA-to-HSA transfers allowed, and the dollar amounts do not count against your annual HSA contribution limit. To make this type of transfer, complete and submit our HSA Transfer Request to your other HSA administrator, or follow their instructions. Forms are available online. Log in and click Resources.

60-day Rollover from Another HSA. You can request a check from your other HSA, if you have one. You must deposit the check into your Gallagher HealthInvest HSA within 60 days. If you fail to do so, the rollover amount will be treated as taxable income and subject to a 20% penalty. This type of rollover is limited to once per 12-month period. The dollar amount does not count against your annual HSA contribution limit. To make a rollover, complete and submit our HSA Rollover Request form to your other HSA administrator, or follow their instructions. Forms are available online. Log in and click Resources.

Qualified Healthcare Expenses

You can use your HSA money for a broad range of medical, dental, and vision expenses that aren’t covered or paid in full by insurance. This includes expenses for your spouse and any qualifying dependents, even if they’re not covered by your high-deductible health plan. Common examples that generally qualify are listed below. Certain restrictions, requirements, or exceptions may apply.

Chiropractic care

Contact lenses, solutions Copays

Deductibles

Dental care (non-cosmetic)

Dentures, adhesives

Eyeglasses

First-aid supplies

Flu shots

Hearing aids

Insulin

Laser eye surgery

Orthodontia

Over-the-counter medicines, products

Physical therapy

Prescriptions

Vision care

In addition, insurance premiums that usually qualify include COBRA, long-term care, health coverage (if on unemployment), and Medicare. For more details, read our What’s Covered one-pager. To get a copy, log in online and click Resources.

Section 213(d) of the Internal Revenue Code defines what is a qualified “medical care” expense. IRS Publication 502 contains guidance that primarily focuses on expenses deductible on tax returns. However, many of the examples it contains also qualify for HSA purposes.

Coordination with an FSA or HRA

Here are several things to keep in mind if you have a general purpose (full coverage) healthcare FSA or HRA in addition to your HSA.

You can have all three types of accounts (HSA, FSA, and HRA).

You can use either account in any order.

However, during any period that you or your spouse make or receive contributions to an HSA, any healthcare FSA or HRA you may have must provide “limited purpose” coverage only, according to IRS rules.

Limited purpose healthcare FSA and HRA coverage is required only for HSA contribution eligibility. If you or your spouse are no longer making or receiving HSA contributions, you can have a general purpose (full coverage) healthcare FSA and/or HRA with no limitations.

“Limited purpose” healthcare FSAs and HRAs may be used for dental- and vision-related expenses. In addition, limited purpose HRAs can be used for qualified high-deductible health plan, dental, and vision premiums.

If you have a Gallagher HealthInvest general purpose (full coverage) healthcare FSA and/or HRA, at open enrollment it will be automatically converted to limited purpose for HSA contribution eligibility purposes. If needed, you can use an FSA or HRA Limited Coverage Election form. Forms for each type of account are available online after logging in and clicking Resources.

Beneficiary Designation

You should name one or more HSA beneficiaries. An HSA beneficiary a person designated to receive all or a portion of your HSA immediately upon your death.

If you name your spouse, your HSA will be transferred to your spouse tax-free.

If you name a non-spouse beneficiary, your HSA will be liquidated and treated as taxable income to that beneficiary.

If you do not name a beneficiary, your HSA will become your spouse’s HSA tax-free. If you have no spouse, your HSA will be liquidated and become taxable on your final tax return, which could cause tax issues.

Beneficiary designations are easy to manage. Log In and click My Profile, then click Beneficiaries. If you prefer, use our Beneficiary Designation form. Forms are available online after logging in and clicking Resources.

Tax Reporting

Certain tax reporting is required as outlined below.

We will furnish you with IRS Form 5498-SA by the end of January if you made or received any contributions during the tax year. We will furnish a second IRS Form 5498-SA in May if you made or received contributions in the new tax year for the previous tax year.

Contributions, if any, made through payroll deduction or otherwise by your employer will be reflected on your IRS Form W-2 in Box 12 (Code W).

We will furnish you with IRS Form 1099-SA by the end of January if you made any withdrawals during the tax year.

You must complete and submit IRS Form 8889 with your tax return.

To view or download copies of your tax forms, log in and click Account Activity, then click View Tax Forms.

If you notice any errors on IRS Form 5498-SA or 1099-SA, contact our Customer Care Center right away at 1-844-342-5505. Immediately contact your employer if your IRS Form W-2 contains an error.